Free cash flow tells you how much cash a business generates after funding the capital spending required to keep the business running and growing. For CFOs, FP&A teams, investors, and operators, this is one of the fastest ways to assess financial flexibility: can the company reinvest, reduce debt, pay dividends, or absorb a downturn without depending on outside capital? If you need to know how to calculate free cash flow accurately, the key is to pull the right figures from the cash flow statement, verify capital expenditures, and avoid mixing profit-based metrics with real cash generation.

All reports in this article are built with FineReport.

Free cash flow, often shortened to FCF, is the cash left over after a company pays for its operating needs and capital expenditures. In plain language, it is the cash the business can use more freely once it has covered the spending required to support operations and long-term assets.

That matters because revenue can look strong while cash is weak. Net income can rise while working capital absorbs cash. A company can even report healthy earnings while still struggling to fund expansion or debt payments. Free cash flow cuts through that noise.

The basic flow is straightforward:

Start with cash from operating activities from the cash flow statement.

Identify capital expenditures from investing activities or disclosures.

Subtract capital expenditures from operating cash flow.

In some cases, you may also use the income statement and balance sheet to validate the result, especially if CapEx is not clearly labeled or if you want to understand what is driving changes in operating cash flow.

Cash Flow vs Profit vs Earnings

These terms are related, but they are not interchangeable:

Profit usually refers to accounting profit after matching revenue and expenses under accrual accounting.

Earnings often refers to net income or EPS-based profitability measures.

Cash flow reflects actual cash moving in and out of the business.

Free cash flow goes one step further by showing cash left after operating needs and capital spending.

A company can be profitable but cash-poor. It can also have temporary positive cash flow while underlying economics are weak. That is why FCF is widely used in credit review, valuation, internal planning, and performance analysis.

Key Metrics (KPIs) to Track Alongside Free Cash Flow

To calculate and interpret FCF properly, finance teams should track these core metrics:

Operating Cash Flow (OCF): Cash generated from core operations before capital spending.

Capital Expenditures (CapEx): Cash spent on property, equipment, software, facilities, or other long-term assets.

Free Cash Flow (FCF): Operating cash flow minus capital expenditures.

Net Income: Accounting profit, useful for comparison but not a substitute for OCF.

Working Capital Change: Movement in receivables, inventory, payables, and other operating accounts that affects cash conversion.

FCF Margin: Free cash flow divided by revenue; shows how efficiently sales convert into discretionary cash.

Cash Conversion Ratio: Operating cash flow divided by net income; helps test earnings quality.

Debt Service Capacity: Indicates whether free cash flow is sufficient to support interest, repayments, or refinancing pressure.

CapEx Intensity: Capital expenditures as a percentage of revenue; helps compare asset-heavy and asset-light models.

FCF Trend: Multi-period direction of free cash flow, often more useful than a single quarter or year.

How to Calculate Free Cash Flow: Formula and Core Components

The standard formula is simple:

Free Cash Flow = Operating Cash Flow - Capital Expenditures

This is the most common version used in practical business analysis and high-level financial review.

Core Components Explained

1. Operating Cash Flow

Operating cash flow, also called cash from operations or CFO/OCF, measures cash generated by the company’s core business activities. It is reported in the operating section of the cash flow statement.

This number already reflects several important realities that earnings do not fully show:

Non-cash items such as depreciation and amortization

Working capital changes

Timing differences in collections and payments

That is why OCF is the right starting point when learning how to calculate free cash flow.

2. Capital Expenditures

Capital expenditures are cash outflows used to acquire, upgrade, or maintain long-term assets. Common examples include:

Machinery and production equipment

Buildings and leasehold improvements

Vehicles and logistics assets

Internal-use software or technology infrastructure

Major facility upgrades

CapEx is usually reported in the investing section of the cash flow statement, often as purchases of property, plant, and equipment.

3. Working Capital Context

Working capital is not directly subtracted again in the simple FCF formula because it is already embedded in operating cash flow. But it still matters for interpretation.

For example:

Rising receivables can reduce OCF even when sales grow

Inventory build-up can pressure cash before revenue is realized

Higher payables can temporarily boost OCF

So while the formula is simple, the business story behind the result often depends on working capital dynamics.

Common Variations Used in Practice

Different analysts use different versions of FCF depending on purpose:

Basic FCF: Operating cash flow minus capital expenditures

Adjusted FCF: Excludes unusual or one-time operating cash movements

Free Cash Flow to Equity (FCFE): Cash available to equity holders after debt-related flows

Free Cash Flow to the Firm (FCFF): Cash available to all capital providers before debt servicing effects

For day-to-day company analysis, the basic version is often enough. For valuation, especially DCF modeling, deeper variations may be more appropriate.

How to Calculate Free Cash Flow: Find the Numbers in Financial Statements

To calculate FCF quickly and correctly, use the financial statements in this order.

Operating Cash Flow on the Cash Flow Statement

Look at the cash flow statement, usually the first section titled:

Cash flows from operating activities

Net cash provided by operating activities

Cash generated from operations

This is your operating cash flow figure.

Capital Expenditures in Investing Activities

Then move to the investing activities section. Look for line items such as:

Purchase of property, plant, and equipment

Additions to fixed assets

Purchase of intangible assets

Capital expenditures

If a company groups items broadly, you may need notes or management discussion to isolate true CapEx.

When the Income Statement and Balance Sheet Help

The income statement and balance sheet improve accuracy when:

CapEx is not clearly disclosed

You want to distinguish maintenance spending from growth spending

You want to understand whether operating cash flow was driven by sustainable operations or working capital swings

You are rebuilding cash flow from raw statements for modeling purposes

For example, PP&E changes on the balance sheet, together with depreciation from the income statement or notes, can help estimate capital expenditures when direct disclosure is limited.

How to Calculate Free Cash Flow: Example Using Financial Statements

Assume a company reports the following for the year:

Net cash from operating activities: $12 million

Purchase of property, plant, and equipment: $4 million

The formula is:

Free Cash Flow = 12million−4 million = $8 million

So the company generated $8 million in free cash flow.

What the Final Figure Means

An 8millionFCFresultmeansthebusinessproduced8 million in cash after funding the capital investments needed during the period. That cash may be used to:

Pay down debt

Build cash reserves

Fund acquisitions

Repurchase shares

Pay dividends

Reinvest selectively in growth

The result is not automatically “good” or “bad” in isolation. Interpretation depends on company size, strategy, growth phase, industry, and trend over time.

A Slightly Deeper Example

Suppose another company reports:

Revenue: $100 million

Net income: $9 million

Operating cash flow: $14 million

Capital expenditures: $11 million

The free cash flow is:

FCF = 14million−11 million = $3 million

This company is profitable, but free cash flow is modest relative to revenue. That may be acceptable if it is in an expansion phase, but it may raise concerns if management claims the business is highly cash-generative.

Common Adjustments to Consider

Experienced analysts often review these adjustments before finalizing FCF:

This is the most common error. Net income is an accrual-based measure. Free cash flow starts with operating cash flow, not earnings.

Missing Capital Expenditures Hidden in Disclosures

Some companies do not label CapEx neatly. It may be embedded in broader investing line items or explained in the notes. If you miss part of it, FCF will be overstated.

Ignoring One-Time Cash Movements

A tax refund, litigation payment, restructuring outflow, or unusual working capital release can distort recurring FCF. Always assess whether the number reflects normal operating performance.

How to Calculate Free Cash Flow: Interpretation and Why It Matters

Once you calculate free cash flow, the next question is what it signals.

What Positive or Negative Free Cash Flow Can Mean

Positive FCF: The company generated cash beyond its operating and capital needs. This usually supports flexibility.

Negative FCF: The company spent more on CapEx than it generated from operations. This is not always a red flag if growth investment is intentional.

Rising FCF: Often signals improving efficiency, stronger cash conversion, or more disciplined capital allocation.

Volatile FCF: May indicate seasonality, cyclical demand, working capital swings, or inconsistent investment timing.

Why Decision-Makers Watch It Closely

Free cash flow matters because it connects operations to strategic options. A company with healthy FCF has more room to:

Reinvest without issuing new equity

Reduce leverage

Manage through downturns

Support shareholder returns

Fund innovation with internal cash

For management teams, this makes FCF a practical operating metric, not just an investor ratio.

Why Trends Matter More Than One Period

A single quarter or year can mislead. One-off CapEx, delayed customer collections, or inventory timing can temporarily distort results. Trend analysis across several periods gives a much better read on:

Earnings quality

Capital intensity

Cash discipline

Resilience under stress

Limits of Free Cash Flow Analysis

Free cash flow is powerful, but it is not complete on its own.

Industry, Business Model, and Growth Stage Matter

A software company and a manufacturer should not be judged by the same FCF profile. Asset-light models often convert more revenue into free cash flow than capital-intensive businesses.

Timing Can Distort the Picture

Seasonality, large facility upgrades, ERP projects, acquisitions, or expansion programs can depress FCF temporarily. That does not necessarily mean the business is underperforming.

Pair FCF with Other Metrics

For a more reliable view, compare free cash flow with:

Revenue growth

Gross and operating margins

Return on invested capital

Debt ratios

CapEx intensity

Working capital efficiency

How to Calculate Free Cash Flow: Uses in Valuation and Decision-Making

Knowing how to calculate free cash flow is useful well beyond reporting. It supports capital allocation, planning, valuation, and risk management.

Practical Business Uses

Organizations use FCF to answer questions like:

Can we fund expansion internally?

How much debt can the business comfortably support?

Is dividend policy sustainable?

Which business units generate real cash after reinvestment?

Are profits translating into liquidity?

For finance leaders, FCF is especially valuable because it links strategy to cash reality.

Free Cash Flow in Valuation

In valuation, free cash flow is central to discounted cash flow analysis. The basic principle is simple: a business is worth the present value of the cash it can generate for its capital providers or shareholders over time.

That is why FCF is often preferred over earnings in valuation work. It is closer to distributable economic value.

Equity-Focused vs Firm-Focused Cash Flow

At a high level:

Basic FCF usually refers to a simple operating cash flow less CapEx view

FCFE focuses on cash available to equity holders

FCFF focuses on cash available to all providers of capital

For operating reviews and quick analysis, basic FCF is usually enough. For formal valuation, FCFF or FCFE may be the better framework.

Actionable Best Practices for Implementing Free Cash Flow Analysis

If you want free cash flow to become a reliable decision metric inside the business, apply it consistently and operationally.

1. Standardize the Definition Across Teams

Decide whether your organization will use:

Reported operating cash flow minus total CapEx

Adjusted operating cash flow minus maintenance CapEx

A separate FCFE or FCFF model for valuation

Do not let FP&A, treasury, and business unit leaders use different definitions without clear labeling.

2. Build a Statement-to-KPI Mapping Process

Create a repeatable workflow that maps:

Cash flow statement operating line items

Investing line items tied to CapEx

Working capital drivers from the balance sheet

Adjustments for unusual items

This reduces inconsistency and speeds monthly and quarterly review.

3. Separate Maintenance and Growth CapEx Where Possible

This is one of the most useful management practices. Maintenance CapEx helps preserve current earnings power. Growth CapEx aims to expand future capacity. If you treat them as one undifferentiated number, you lose strategic insight.

4. Review FCF Trends with Operational Drivers

Do not report free cash flow as a standalone figure. Pair it with:

DSO, DIO, and DPO

Capacity utilization

Margin trends

Project spend

Revenue quality by segment

This turns FCF from a finance metric into an operating control metric.

5. Use Dashboards for Multi-Period Monitoring

A strong dashboard should show:

Current-period FCF

Rolling 12-month FCF

CapEx trend

Working capital changes

Variance to plan

Segment or entity comparison

How to Calculate Free Cash Flow: Uses in Valuation and Decision-Making

Free cash flow should influence more than investor presentations. It should shape everyday management choices.

Budgeting and Capital Allocation

Finance teams use FCF to determine:

Whether planned investments are affordable

How much financial headroom exists

Which projects are generating acceptable cash returns

Whether growth is creating value or just consuming liquidity

This is especially important in capital-intensive sectors where earnings may look stable but cash demands are heavy.

Financing and Debt Decisions

Lenders and internal treasury teams watch free cash flow because debt is repaid with cash, not accounting earnings. A company with consistently weak FCF may face tighter borrowing conditions even if reported profit appears acceptable.

Performance Management

At the enterprise level, FCF helps assess whether management is:

Turning revenue into usable cash

Investing at the right pace

Controlling working capital

Preserving flexibility under uncertainty

Get Ready-to-Use Dashboard Templates in Fine Gallery

Free Cash Flow to Firm and Related Variations

What Is FCFF?

Free cash flow to the firm, or FCFF, is the cash flow available to all capital providers, including both debt and equity. Analysts often use FCFF in enterprise valuation models because it reflects pre-financing cash generation.

FCFF vs Basic FCF

Basic FCF is excellent for quick analysis and business monitoring. FCFF is better when you need to value the full enterprise consistently, especially across companies with different capital structures.

When a Deeper Model Is Worth It

Use a more advanced FCFF or FCFE approach when:

You are building a DCF model

Capital structure matters materially

The business has volatile leverage

You need investor-grade valuation outputs

Use the simple FCF approach when:

You are doing internal performance review

You need a quick liquidity test

You are comparing cash generation across periods

Reported statements already provide clean OCF and CapEx data

Key Takeaways and a Practical Checklist

The basic formula is simple:

Free Cash Flow = Operating Cash Flow - Capital Expenditures

But a reliable calculation depends on using the right statement inputs, checking disclosures carefully, and interpreting the result in context.

Practical Checklist for Calculating Free Cash Flow

Use this checklist each time:

Find operating cash flow on the cash flow statement.

Locate capital expenditures in investing activities or supporting notes.

Subtract CapEx from operating cash flow to calculate FCF.

Verify that CapEx is complete and not buried in broader line items.

Check for unusual one-time cash items affecting operating cash flow.

Review working capital movements to understand what drove the result.

Compare multiple periods, not just one quarter or year.

Assess FCF against revenue, margins, and debt needs for context.

Separate maintenance and growth CapEx if decision-making requires deeper insight.

Use disclosures and management commentary to validate interpretation.

A clean free cash flow calculation can reveal far more than a profit figure alone. It shows whether the business is actually producing usable cash after reinvestment. That is why it remains one of the most practical metrics in finance, operations, and valuation.

The standard formula is free cash flow equals operating cash flow minus capital expenditures. It shows how much cash remains after the business funds its core operations and long-term asset investments.

Operating cash flow is usually listed in the operating activities section of the cash flow statement. Capital expenditures are typically found in the investing activities section, often under purchases of property, plant, and equipment.

Net income is based on accrual accounting, while free cash flow focuses on actual cash generated after capital spending. A company can report strong earnings but still have weak free cash flow if cash is tied up in working capital or heavy investment.

Yes, negative free cash flow is not always a bad sign if the company is investing heavily for future growth. The key is to determine whether the cash outflow comes from productive expansion or from weak underlying operations.

Analysts use free cash flow to assess liquidity, debt capacity, reinvestment potential, and overall financial flexibility. It is also a core input in valuation methods such as discounted cash flow analysis.

Product Trial

FineReport

Pixel-perfect reports · Interactive dashboards · Easy data entry · Digital twins

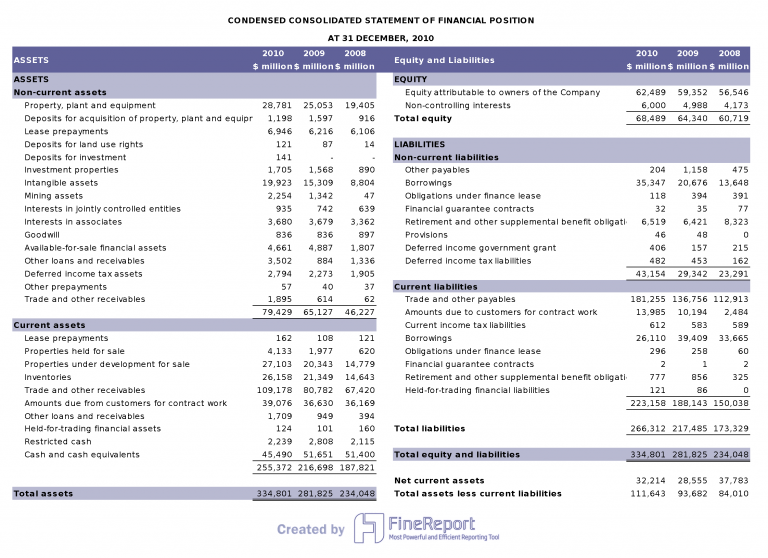

Balance Sheet made by

Balance Sheet made by