Internal controls over financial reporting are the policies, procedures, reviews, and system-based safeguards that help organizations produce reliable financial statements, support timely disclosures, and reduce the risk of material misstatement. For CFOs, controllers, internal audit leaders, compliance teams, and audit committees, ICFR is not a theory exercise. It is the operating discipline that determines whether close processes hold up under pressure, whether journal entries are defensible, whether spreadsheets can be trusted, and whether auditors will find gaps that create delays, rework, or serious reporting issues.

Click To Try The Dashboard

All reports in this article are built with FineReport

What internal controls over financial reporting means in practice

In practice, internal controls over financial reporting are the mechanisms management uses to gain reasonable assurance that financial reporting is complete, accurate, authorized, and compliant with the applicable reporting framework. A strong ICFR program helps leaders answer critical questions quickly: Are our balances supportable? Are disclosures complete? Can we detect errors before filing deadlines? Can we prove controls operated as intended?

For finance leaders, the business value is straightforward:

Fewer reporting surprises during close and audit

Lower risk of restatements and disclosure failures

Better accountability across finance, IT, and operations

Faster remediation when exceptions occur

More confidence in board, lender, and investor reporting

ICFR typically includes three major control layers:

Entity-level controls

These are top-down controls that influence the overall control culture and governance structure of the company. They include executive oversight, code of conduct, audit committee governance, policy approval, whistleblower channels, and financial reporting accountability.

Entity-level controls matter because weak governance often undermines every downstream control, even when process documentation looks complete on paper.

Process-level controls

These controls operate inside specific financial reporting cycles such as revenue, accounts payable, treasury, and close and consolidation. Examples include reconciliations, approval workflows, review controls, and exception monitoring.

Process-level controls are where many reporting risks are actively prevented or detected.

IT-dependent controls

These controls rely on systems, reports, interfaces, and application logic. They include access management, change management, automated validations, report-based review controls, and system-generated exception alerts.

If management relies on data or system reports to perform a control, the integrity of that data source becomes part of the control framework.

The core objective of ICFR

The objective is not perfection. It is reasonable assurance that the company can produce reliable financial statements and timely disclosures, and that material errors are prevented or detected in time to be corrected.

Key Metrics (KPIs) for an ICFR program

Below are the most useful KPIs finance and audit leaders should track:

Control coverage rate: Percentage of key financial reporting risks mapped to documented controls.

Testing completion rate: Share of planned control tests completed within the reporting period.

Operating effectiveness rate: Percentage of tested controls that operated as designed without exception.

Deficiency count by severity: Number of deficiencies categorized as control deficiency, significant deficiency, or material weakness.

Remediation cycle time: Average number of days required to close identified control issues.

Repeat deficiency rate: Percentage of issues that recur after prior remediation.

Close process exception rate: Number of close-related errors, late adjustments, or unsupported balances identified during period-end close.

Access violation count: Number of unresolved segregation of duties or privileged access exceptions affecting financial systems.

Spreadsheet risk exposure: Volume of high-risk manual spreadsheets used in key reporting processes.

Evidence timeliness: Percentage of controls with complete, review-ready evidence retained on time.

The core components of an effective ICFR framework

An effective ICFR framework is built on governance, risk-based design, disciplined execution, and monitoring. The strongest programs do not document everything equally. They focus on what could cause a material misstatement and prove that the right controls are in place.

Control environment and governance

The control environment sets the baseline for every financial reporting decision. If leadership tolerates sloppy review practices, unclear ownership, or inconsistent escalation, even well-written controls will fail.

A sound governance structure usually includes:

Clear accountability from the CFO, controller, and process owners

Audit committee oversight of reporting quality and remediation progress

Formal financial reporting policies and close calendars

Defined approval authorities and review responsibilities

Expectations for ethical conduct and escalation of issues

Strong tone at the top shows up in operational behaviors, not slogans. Examples include timely review of reconciliations, challenge of unusual transactions, documented sign-offs, and prompt escalation of unresolved issues.

Risk assessment and control design

The best ICFR programs start with risk, not templates. Management should identify the accounts, disclosures, transaction classes, and assertions that could lead to a material misstatement.

That means evaluating:

Material accounts and disclosures

Relevant assertions such as completeness, accuracy, valuation, existence, rights and obligations, and presentation

Fraud risk factors

Non-routine and judgmental transactions

Risks introduced by system changes, acquisitions, or manual workarounds

From there, controls should be designed to address the specific risk with enough precision. A vague review control is rarely sufficient. A well-designed control specifies who performs the review, what they inspect, what threshold they use, how exceptions are resolved, and what evidence is retained.

Core Elements of effective control design

Risk linkage: Each key control should address a defined reporting risk.

Precision: The control must be specific enough to catch material errors.

Frequency: Control timing should align with the risk exposure.

Ownership: A named control owner must be accountable for performance.

Evidence: Execution must leave a clear audit trail.

System reliance: Data sources and reports used in the control must be trustworthy.

Escalation path: Exceptions must trigger documented follow-up.

Information, communication, and monitoring

Even well-designed controls break down when documentation is fragmented or issues stay trapped within departments. ICFR requires information to move fast and clearly across finance, IT, internal audit, compliance, and executive leadership.

At a minimum, organizations need:

Standardized documentation formats

Defined evidence retention practices

Timely issue escalation protocols

Periodic control testing and status reporting

Continuous improvement based on findings and recurring exceptions

Monitoring should not happen only at year-end. Mature organizations review control health throughout the year, especially around major business changes, ERP updates, restructurings, and close process bottlenecks.

How to build and document an ICFR program step by step

Building an ICFR program requires disciplined scoping, process understanding, and practical documentation. The goal is to create a framework that stands up to management review and external audit without becoming administratively impossible to maintain.

Scope the financial reporting processes that matter most

Start with a top-down, risk-based scoping exercise. Not every entity, account, or process needs the same level of attention.

Focus first on:

High-risk legal entities and business units

Significant accounts and disclosures

Processes involving high judgment or estimation

Areas with known audit issues or control history

Systems and interfaces feeding the general ledger

Common scoping mistakes include documenting low-risk activity in excessive detail while under-documenting complex estimates, journal entries, consolidation adjustments, and IT dependencies.

Map risks to controls across major processes

Once scope is defined, map each key financial reporting risk to the controls that prevent or detect it. This is where many programs either become strong or become cluttered.

A practical example: if management reviews a monthly revenue trend report to identify unusual variances, the documentation should specify the report used, the thresholds investigated, the preparer and reviewer, how anomalies are resolved, and where the evidence is stored.

Prepare documentation that stands up to review

The most defensible ICFR programs use documentation that is clear, current, and easy to trace from risk to control to evidence.

Essential artifacts include:

Process narratives: Plain-language descriptions of how transactions flow and where controls occur.

Flowcharts: Visual process maps showing handoffs, approvals, and system touchpoints.

Risk-control matrices: Structured mapping of risks, assertions, controls, ownership, and test approach.

Control inventory: Master list of key controls, frequencies, owners, and dependencies.

Evidence retention standards: Rules for naming, storing, versioning, and retrieving support.

Issue logs and remediation trackers: Centralized record of identified deficiencies and action plans.

Testing, auditing, and remediating ICFR deficiencies

Testing is where documented controls meet operational reality. This is also the stage where management learns whether controls are truly embedded or merely described.

How management evaluates operating effectiveness

Management typically evaluates two things:

Design effectiveness: Whether the control, if performed as designed, would address the risk

Operating effectiveness: Whether the control actually operated consistently during the period

A control can be well designed and still fail in practice because reviews were rushed, evidence was incomplete, or exceptions were not resolved.

Sample-based testing is commonly used for recurring controls. The size and nature of samples depend on control frequency, risk, and prior results. High-risk controls, manual controls, and controls with a history of failure generally deserve more rigorous testing.

Practical testing steps include:

Confirm the control description and risk linkage

Inspect whether the control design is sufficiently precise

Select samples covering the period under review

Examine evidence of execution and reviewer challenge

External and internal auditors look beyond checkbox completion. They want evidence that the control owner understood the purpose of the control, performed it at the right time, used complete and accurate information, and resolved exceptions appropriately.

Auditors often focus on:

Walkthroughs from transaction initiation to financial statement impact

Evidence that key controls occurred at the stated frequency

Re-performance of selected controls

Review signatures, dates, and documented follow-up

Reliability of reports used in review controls

IT general controls that support automated or report-based controls

If an exception is found, auditors assess whether it indicates a one-off lapse, a broader control failure, or a risk that material misstatements could go undetected.

Remediation plans for control gaps and material weaknesses

Not all deficiencies are equal. Some can be fixed quickly with better documentation or training. Others reveal structural weaknesses in systems, staffing, governance, or process design.

Effective remediation usually follows this sequence:

Prioritize by severity and exposure: Address issues affecting material accounts, key disclosures, or pervasive controls first.

Perform root-cause analysis: Determine whether the issue stems from design, execution, unclear ownership, poor data, or system limitations.

Implement corrective actions: Redesign controls, automate steps, improve review precision, or add compensating controls where necessary.

Retest after remediation: Confirm the revised control operated effectively for a sufficient period.

Track closure centrally: Maintain clear evidence that management reviewed and approved closure.

A common failure is treating remediation as a paperwork exercise. If the root cause is manual overload, weak system access governance, or lack of accounting expertise, the fix must address the operating model, not just the form.

Reporting responsibilities and leadership accountability

ICFR works only when leadership treats it as an ongoing management responsibility rather than a year-end compliance project.

Management reporting and annual assessments

Management is generally responsible for assessing the effectiveness of internal controls over financial reporting and supporting that conclusion with evidence. In practice, this means leaders should be able to explain:

The framework used to evaluate ICFR

The scope of the assessment

The results of testing performed

Significant deficiencies or material weaknesses identified

Remediation status and unresolved risks

Disclosure implications for annual and interim reporting

This responsibility usually sits with senior finance leadership, but it depends on coordinated input from IT, compliance, legal, internal audit, and business process owners.

The audit committee should have visibility into the health of the control environment, major risks, and unresolved deficiencies. They do not run the control program, but they provide oversight, challenge management, and monitor whether remediation is happening with urgency.

Cross-functional ownership is essential because ICFR often fails at handoff points. Finance may own reconciliation reviews, but IT may own access rights, HR may own role changes, and operations may initiate transactions that drive accounting results.

A practical ownership model often includes:

Finance: Process ownership, reconciliations, close controls, disclosure controls

IT: Access controls, change management, report integrity, system interfaces

Compliance and legal: Policy support, escalation protocols, governance coordination

Business process owners: Front-line execution of operational controls with financial reporting impact

Common ICFR challenges and practical ways to strengthen controls

Most ICFR breakdowns are not caused by lack of intent. They are caused by operational friction, unclear ownership, poor evidence discipline, and overreliance on manual work.

Common challenges include:

Manual controls that depend on one experienced individual

Spreadsheet-heavy processes with weak version control

Segregation of duties conflicts in lean teams

ERP changes that outpace control redesign

Review controls with vague criteria or weak evidence

Incomplete documentation of report logic or system dependencies

Delayed remediation that turns deficiencies into recurring issues

4 best practices from the field

These are the habits I recommend most often to finance and audit leaders building sustainable ICFR programs:

1. Standardize evidence before auditors ask for it

Create naming conventions, repository rules, reviewer sign-off requirements, and retention schedules. Poor evidence management is one of the fastest ways to make a functioning control look ineffective.

2. Reduce manual control load in high-risk areas

Where possible, automate reconciliations, workflow approvals, exception alerts, and certification tasks. Manual controls are harder to scale, test, and sustain during staffing changes.

3. Reassess scoping after every major business change

Acquisitions, reorganizations, new systems, outsourcing, and product launches can change financial reporting risk quickly. Update the ICFR scope before year-end, not after issues surface.

4. Track remediation like an operating KPI

Assign owners, due dates, root causes, and retest milestones. Review remediation progress in recurring governance meetings, not as a side spreadsheet.

After best practices, many organizations hit the same reality: building this manually across entities, controls, evidence, testing, and dashboards becomes slow and difficult to govern.

Level 1 – Reactive: Controls are informal, documentation is scattered, and testing is largely audit-driven.

Level 2 – Defined: Key processes are documented, major controls are identified, but evidence and remediation are inconsistent.

Level 3 – Managed: Risk-control matrices, periodic testing, issue tracking, and governance routines are established.

Level 4 – Integrated: Finance, IT, and audit work from a shared control framework with centralized reporting and stronger automation.

Level 5 – Optimized: Control monitoring is continuous, dashboards are real-time, and control improvements are tied to close efficiency and reporting quality.

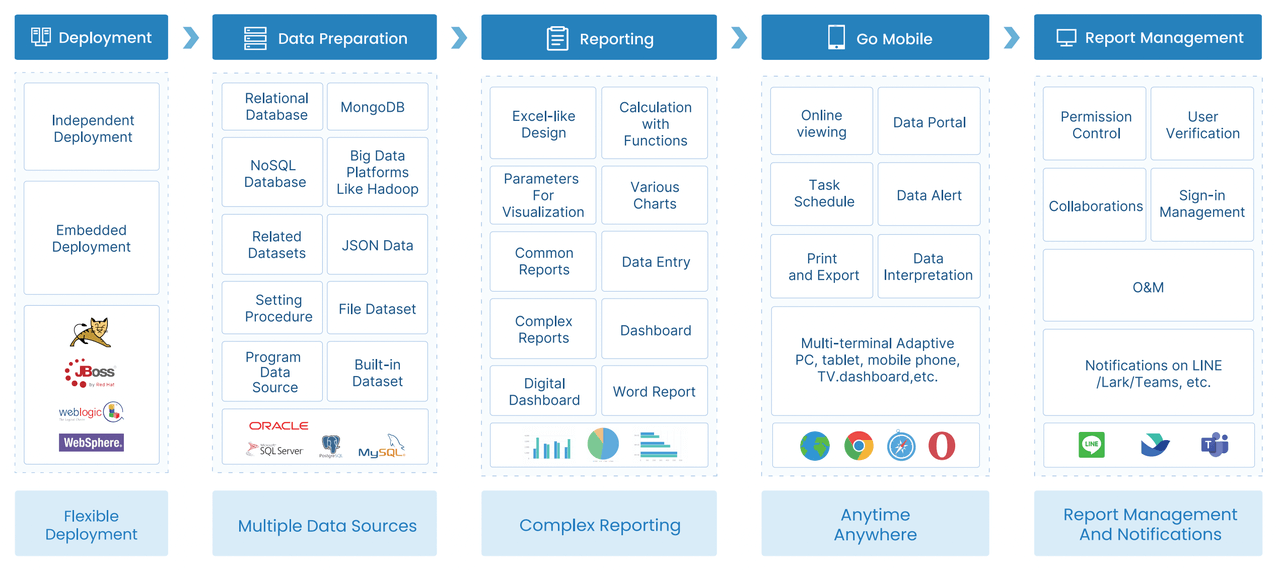

From framework to execution: automate internal controls over financial reporting with FineReport

Building this manually is complex; use FineReport to utilize ready-made templates and automate this entire workflow. For enterprise teams managing internal controls over financial reporting, the real challenge is not just defining controls. It is turning control status, testing results, remediation progress, and management reporting into one visible, auditable operating system.

FineReport helps teams do that by centralizing control dashboards, integrating data from ERP and finance systems, standardizing reporting outputs, and reducing the spreadsheet burden that weakens many ICFR programs. Instead of chasing status updates across email threads and offline trackers, leaders can monitor testing coverage, deficiencies, overdue actions, and close-related risks in one place.

Get Ready-to-Use Dashboard Templates in Fine Gallery

This matters especially when your organization needs to:

Consolidate ICFR reporting across multiple entities or business units

Visualize control gaps by process, owner, or severity

Track remediation plans with accountability and due dates

Present management and audit committee updates with confidence

Build repeatable, audit-ready evidence trails

A modern ICFR program should not rely on disconnected files and last-minute status collection. It should run on governed data, clear ownership, and reporting automation that gives leadership an accurate view of control health at any time.

If your team is ready to strengthen control visibility, reduce manual reporting effort, and build a more sustainable ICFR operating model, FineReport is the practical next step.

Internal control over financial reporting, or ICFR, is the system of policies, reviews, approvals, and technology checks that helps a company produce accurate and reliable financial statements. Its purpose is to provide reasonable assurance that material errors or unauthorized transactions are prevented or detected in time.

ICFR is the control framework itself, while SOX is the regulatory law that requires certain companies to assess and report on those controls. In practice, SOX compliance often depends on how well an organization designs, tests, and maintains its ICFR program.

A strong ICFR framework usually includes entity-level controls, process-level controls, and IT-dependent controls. These work together to support governance, reduce reporting risk, and strengthen the reliability of financial data.

Companies evaluate ICFR through control testing, monitoring of exceptions, review of supporting evidence, and tracking of remediation efforts. Common indicators include testing completion, operating effectiveness, deficiency severity, and repeat issues.

Frequent weaknesses include poor segregation of duties, incomplete reconciliations, unreliable spreadsheets, weak access controls, and missing review evidence. These gaps can increase the risk of material misstatement, audit delays, and remediation costs.

Product Trial

FineReport

Pixel-perfect reports · Interactive dashboards · Easy data entry · Digital twins