A variance analysis report should help leadership make faster, better decisions—not force them to decode finance spreadsheets. For CFOs, FP&A leaders, controllers, and business unit heads, the real challenge is not calculating variances. It is turning those numbers into a short, credible, decision-ready report that highlights what changed, why it matters, and what needs action now.

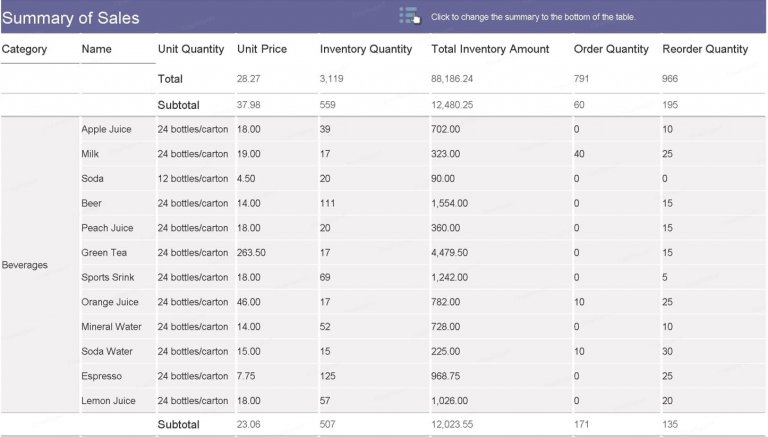

Click To Try The Dashboard

All reports in this article are built with FineReport

What a variance analysis report is and why executives care

A variance analysis report compares actual results against a benchmark such as budget, forecast, prior period, prior year, or target. In plain language, it shows where performance deviated from plan and explains what caused that gap.

Executives care because the report answers three high-value questions quickly:

Where are we off plan?

Why did it happen?

What decision is required now?

Raw financial variance data alone is not enough. A spreadsheet full of account-level movements may be technically accurate, but it is not useful to leadership unless it is prioritized, interpreted, and linked to business action. Decision-ready reporting filters out noise, focuses on material changes, and connects financial movement to operational causes like pricing, volume, productivity, timing, or one-off events.

Key Metrics (KPIs) executives expect in a variance analysis report

A strong report usually includes a focused set of metrics rather than every line item in the chart of accounts.

Revenue Variance: Difference between actual revenue and plan. Signals demand, pricing, sales execution, or timing issues.

Gross Margin Variance: Change in margin versus benchmark. Helps reveal pricing pressure, product mix shifts, or cost inflation.

Operating Expense Variance: Difference in spend across departments or cost centers. Highlights overspending, underinvestment, or timing delays.

EBITDA or Operating Profit Variance: Measures how performance changes are affecting profitability at a leadership level.

Cash Flow Variance: Compares actual cash generation or usage to plan. Critical for liquidity, runway, and working capital decisions.

Volume Variance: Shows the impact of selling or producing more or fewer units than expected.

Price Variance: Measures the effect of actual selling price or input cost versus assumed price.

Mix Variance: Explains how changes in product, customer, or channel mix affect total results.

Timing Variance: Distinguishes delays or accelerations from true performance changes.

Forecast Accuracy: Tracks how closely prior forecasts matched actual outcomes, improving planning discipline.

The essential sections of a variance analysis report executives actually use

Start with an executive summary

The executive summary is the most important part of the report because most senior leaders will read it first—and sometimes only it. It should lead with the largest business drivers, the estimated impact, and the decisions needed.

A useful summary should answer:

What changed versus budget, forecast, prior period, or target?

Which 3 to 5 variances matter most?

Are they favorable or unfavorable?

What is the likely business impact?

What action or escalation is needed?

Instead of saying, “Operating expenses were 8% over budget,” say, “Operating expenses were $1.2M over budget, driven primarily by contractor spend in IT and expedited freight in operations; CFO approval is needed on whether to absorb, reallocate, or cut elsewhere.”

Executives do not need a full ledger dump. They need material exceptions. That means focusing on meaningful gaps in:

Revenue

Cost of goods sold

Gross margin

Operating expenses

EBITDA

Cash flow

Critical operational KPIs

Separate favorable and unfavorable movements visually and explain them in business language. A favorable variance is not always good news. For example, underspending in hiring may look positive but can indicate delayed growth capacity. Likewise, a negative cost variance may be acceptable if it supported stronger-than-expected revenue.

A useful rule: if a variance does not change a decision, it probably does not belong in the main report.

Add commentary that explains the story

Numbers do not persuade executives on their own. Commentary does. The best reports connect the variance to root causes and implications.

Common root-cause categories include:

Pricing

Volume

Product or customer mix

Timing

Labor efficiency

Supplier cost changes

One-time events

Execution gaps

Market shifts

Good commentary follows a simple pattern:

What happened

Why it happened

What it means

What happens next

For example:

Revenue was 6% below forecast.

The shortfall came mainly from lower enterprise deal volume in the West region.

This reduces quarterly margin leverage and pushes back cash collection.

Sales leadership will review pipeline conversion and submit a recovery plan by next Friday.

That is far more useful than “sales unfavorable due to volume.”

How to read variance analysis the way leadership teams do

Identify what matters most first

Leadership teams scan for magnitude, trend, risk, and controllability. They want to know which issues are biggest, whether they are recurring, how much they threaten performance, and whether management can actually act on them.

To make that easier, apply materiality thresholds such as:

Dollar threshold, for example variances above $100,000

Percentage threshold, for example above 10%

Strategic threshold, for example anything affecting cash runway, gross margin, or customer retention

These thresholds help distinguish signal from noise. Without them, teams waste time discussing immaterial fluctuations.

Executives rarely evaluate a variance in isolation. They compare it across multiple lenses:

Actual versus budget

Actual versus latest forecast

Actual versus prior month

Actual versus prior year

Actual versus scenario plan

This multi-view approach shows whether a problem is new, recurring, seasonal, or improving. It also helps separate planning error from execution error.

For example, if revenue missed budget but beat the latest forecast, the story changes. The business may still be recovering. If gross margin is down but volume is up, the next question becomes whether discounting or mix drove the growth.

Strong leadership teams also want accountability. Each major variance should map to an owner, a business process, or a department.

The point of a variance analysis report is not explanation alone. It is action.

Every major section should make clear:

What decision is needed

Who owns the follow-up

What deadline applies

Whether the issue needs escalation

A report becomes useful when it supports actions like:

Freeze nonessential spend

Reforecast revenue and margin

Renegotiate supplier contracts

Adjust hiring plans

Shift budget between business units

Escalate performance risk to the executive committee

If your report ends with commentary but no owner or timeline, it is incomplete.

How to write a variance analysis report step by step

Define the reporting objective and audience

Start by identifying who will read the report and what they need from it.

Different audiences want different levels of detail:

CEO: Strategic impact, trends, and key decisions

CFO: Financial drivers, risk, forecast implications, and control actions

Business unit leader: Operational causes, team performance, and corrective steps

Board member: Material variances, risk exposure, and management response

Also clarify whether the report is meant to:

Inform

Diagnose

Drive action

That choice affects structure, detail level, and tone. A board report should be concise and strategic. A business review report can go deeper into operational drivers.

Not every benchmark fits every situation. Pick comparisons based on the decision context.

Common frameworks include:

Actual vs Budget: Best for measuring execution against plan

Actual vs Forecast: Best for short-term management and course correction

Actual vs Prior Month: Best for recent trend analysis

Actual vs Prior Year: Best for seasonality and year-over-year performance

Actual vs Scenario Plan: Best for uncertainty, stress testing, or strategic alternatives

The most important principle is consistency. If comparison periods keep changing, trend interpretation becomes unreliable and executives lose confidence in the report.

You may also use common variance types when helpful:

Price variance

Volume variance

Mix variance

Rate variance

Efficiency variance

Timing variance

The goal is not to impress readers with technical decomposition. The goal is to explain performance clearly. Use advanced formulas only when they materially improve understanding.

Common mistakes and a practical template to get started

Mistakes that make executives ignore the report

Many variance reports fail not because the numbers are wrong, but because the reporting is poorly designed.

Common mistakes include:

Presenting too much detail without clear priorities

Listing every variance instead of only material ones

Explaining numbers without naming owners or deadlines

Mixing inconsistent data sources or comparison periods

Using finance jargon instead of business language

Showing variances without context on risk, trend, or actionability

Treating favorable variances as automatically positive

Delivering reports too late to influence decisions

A report executives ignore is usually one that makes them do too much interpretation themselves.

A simple template for your next report

A practical executive-ready variance analysis report can follow this structure:

1. Executive Summary

Top 3 to 5 variances

Business impact

Decisions required

Escalations

2. Top Variances and Drivers

Revenue

Cost

Margin

Cash flow

Operational KPI exceptions

3. Root-Cause Commentary

What happened

Why it happened

Whether it is timing, structural, or one-time

Forecast implications

4. Actions, Owners, and Follow-Up Timeline

Recommended action

Accountable team

Due date

Status

Build the report once, automate it with FineReport

Building this manually is complex; use FineReport to utilize ready-made templates and automate this entire workflow.

FineReport helps finance and operations teams turn scattered actuals, budgets, forecasts, and KPI data into executive-ready variance analysis reports with less manual effort. Instead of stitching together spreadsheets every month, teams can standardize layouts, automate calculations, refresh data from multiple systems, and distribute role-based reports to CEOs, CFOs, and department leaders.

That matters because executive reporting is not just about presentation. It depends on repeatable logic, governed data, drill-down capability, and fast turnaround. FineReport supports that with:

It should include a brief executive summary, the most material variances, clear root-cause commentary, business impact, and the action or decision required. Executives want the report to show what changed, why it matters, and what needs to happen next.

A standard spreadsheet shows raw numbers, while an executive-ready variance report prioritizes only the most important exceptions and explains them in business terms. The goal is faster decision-making, not more detail.

The most useful KPIs usually include revenue, gross margin, operating expenses, EBITDA or operating profit, cash flow, and key operational drivers like price, volume, mix, and timing. The exact mix should reflect what leadership uses to make decisions.

Most companies produce them monthly, with quarterly views for broader strategic review. If the business is changing quickly, more frequent reporting may be needed to catch issues early.

Focus on material variances, use plain language, separate timing issues from true performance problems, and connect each variance to a recommended action. Tools like FineReport can also help present the information in a clearer dashboard format.

Product Trial

FineReport

Pixel-perfect reports · Interactive dashboards · Easy data entry · Digital twins