Financial institutions run on data. Customer records, transactions, risk models, product data, collateral details, claims, positions, and regulatory submissions all depend on information being accurate, consistent, secure, and traceable. That is exactly why data governance financial services programs have moved from “nice to have” to operational necessity.

For beginners, the term can sound abstract. In practice, it is not. Data governance is simply the set of decisions, rules, roles, and controls that help a bank, insurer, lender, or investment firm treat data as a managed business asset.

This guide explains what data governance means in financial services, why it matters, how the core framework works, and how to get started without overengineering the effort.

What Data Governance in Financial Services Means

In financial services, data governance is the discipline of deciding:

What key data means

Who owns it

Who can use it

How quality is measured

How issues are fixed

How rules are enforced over time

For a bank, this may apply to customer identity, account status, exposure, default definitions, transaction records, and regulatory reporting fields. For an insurer, it may cover policyholder data, claims, underwriting attributes, and actuarial inputs. For lenders and investment firms, it often includes pricing data, risk metrics, portfolio attributes, and counterparty information.

Put simply, data governance financial services programs create order around critical data so the business can trust it.

Data governance is often confused with adjacent functions. They are related, but not the same.

A useful way to think about it: governance sets the rules, management executes them, compliance checks obligations, security protects access, and analytics uses the output.

This distinction matters because financial firms often assume they already have governance when they really have fragmented data operations, isolated controls, or reporting committees without clear ownership.

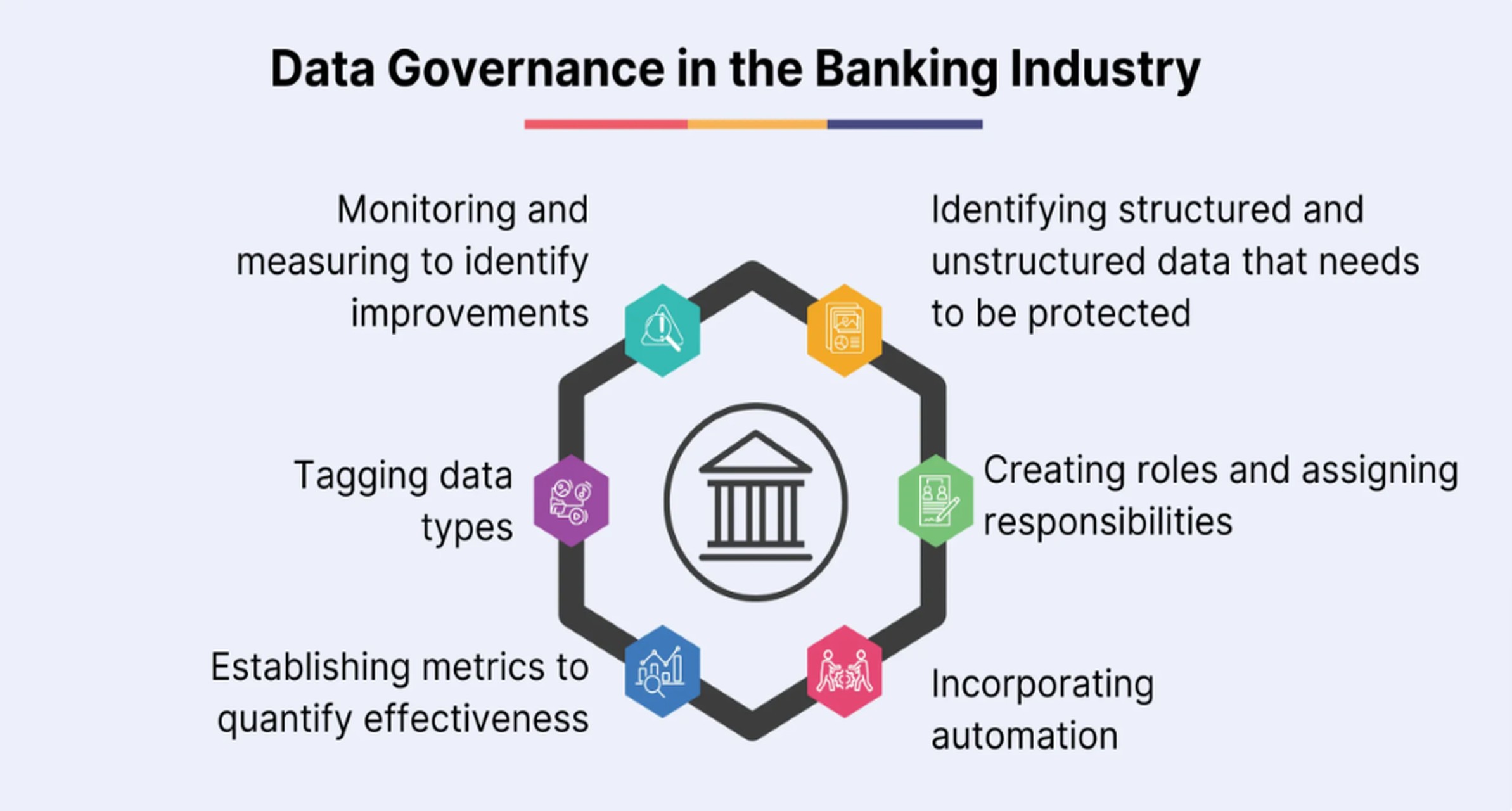

Highly regulated financial data needs more than storage and reporting. It needs:

Clear ownership so definitions do not drift across departments

Common standards so metrics remain consistent across systems and reports

Controls so sensitive data is used properly

Traceability so teams can explain where data came from and how it changed

Escalation paths so quality issues are resolved before they become audit or regulatory problems

When those elements are missing, every downstream process suffers: onboarding slows down, risk reports conflict, audit findings increase, and executive decisions become less reliable.

Why Data Governance Matters for Financial Services

Financial firms face a simple problem with complex consequences: they depend on data to make high-stakes decisions, yet that data is often scattered across legacy systems, manual spreadsheets, vendor feeds, and business silos.

That is why data governance matters. It helps institutions reduce risk while improving day-to-day performance.

Risk reduction and regulatory readiness

In financial services, poor data quality is not just inconvenient. It can lead to:

Incorrect regulatory reports

Faulty credit or risk assessments

Incomplete KYC records

Delayed investigations

Weak audit trails

Customer complaints

Fines, remediation costs, and reputational damage

Strong governance improves regulatory readiness by ensuring that critical data elements are defined, controlled, and monitored. When regulators, auditors, or internal control teams ask how a number was produced, the organization can answer with confidence.

Customer trust

Customers expect financial institutions to handle their information carefully and accurately. When addresses are wrong, customer risk ratings conflict across systems, or service teams cannot see the same profile, trust erodes quickly.

Governance supports trust by improving consistency across customer-facing processes such as onboarding, servicing, lending, claims, and digital interactions.

Better decision-making

Executives, risk leaders, finance teams, and frontline managers all rely on reports and dashboards. But reporting is only as strong as the underlying data definitions and controls.

Without governance, one department’s “active customer” may not match another’s. One report may define delinquency differently from another. These inconsistencies create debate instead of action.

With governance, decision-makers spend less time arguing over the numbers and more time responding to what the numbers mean.

Common pain points in financial institutions

Most beginners recognize data governance is needed when they see symptoms like these:

Siloed systems that store different versions of the same customer or product

Inconsistent reporting across finance, risk, compliance, and operations

Poor data quality, including duplicates, missing fields, and outdated values

Manual reconciliations that absorb time each month or quarter

Unclear accountability for fixing data issues

Access permissions that are too broad or poorly documented

Weak data lineage for key reports and models

These are not only technical issues. They are governance issues because they reflect missing standards, unclear ownership, and weak operating discipline.

The business value of a stronger finance data strategy

A mature governance model does more than support compliance. It also creates business value through:

This is where platforms such as FineBI can become useful. Once governance establishes trusted definitions, ownership, and quality expectations, BI tools can expose consistent metrics to business users in a controlled and self-service way. Governance makes insight trustworthy; BI makes it usable.

Core Frameworks for Building a Data Governance Financial Services Program

A practical data governance financial services framework does not need to start large. But it does need to cover four essentials: policies, roles, processes, and oversight.

Policies, standards, and controls

Policies and standards are the written foundation of governance. They explain how data should be defined, handled, protected, retained, and reviewed.

At minimum, beginners should understand these document types:

Manages day-to-day governance tasks, standards, and issue coordination

Compliance and risk teams

Align governance with regulatory and control expectations

IT and architecture teams

Support metadata, lineage, integration, access, and technical controls

Business users

Follow policies, raise issues, and use governed data correctly

For beginners, the most important distinction is this:

Data owners are accountable

Data stewards are operationally responsible

IT enables but does not own business meaning

Compliance advises and challenges, but should not be the only governance driver

A common mistake is assigning everything to IT. In financial services, business ownership is critical because product, risk, finance, operations, and compliance teams understand the meaning and consequences of the data.

Processes and operating model

Policies and roles matter only if they are supported by repeatable processes. A workable governance operating model usually includes the following processes:

Issue management

When a data defect appears, the organization should know:

How the issue is logged

Who triages it

How severity is determined

Who approves remediation

When escalation is required

How closure is verified

This avoids the common problem of data issues being discussed repeatedly with no owner and no resolution date.

Data quality workflows

Data quality should be monitored through defined checks such as:

Completeness

Accuracy

Validity

Timeliness

Consistency

Uniqueness

A mature process does not just identify bad data. It also traces root cause and prevents recurrence.

Access reviews

Financial data access must be reviewed regularly, especially for:

Without lineage, teams struggle to explain transformations, reconcile changes, or defend calculations during audit.

Escalation paths

Not all data issues are equal. A missing optional field in a low-risk process is not the same as a broken feed affecting capital or suspicious activity monitoring. Governance should define escalation thresholds by impact, risk, and urgency.

Metrics and oversight

What gets measured gets managed. Governance programs need a small set of clear indicators.

Useful beginner metrics include:

Percentage of critical data elements with assigned owners

Percentage of approved definitions published

Data quality scores by domain

Number of open issues and aging trends

Remediation time by severity

Policy adoption by business unit

Number of access reviews completed on time

Lineage coverage for critical reports

Audit findings related to data controls

These metrics should be reviewed by a governance forum or steering committee with enough authority to unblock decisions.

Good oversight is not about creating more meetings. It is about making accountability visible.

How Data Governance Works in Financial Services: Use Cases

The easiest way to understand governance is to see it in business use cases.

Customer onboarding

Customer onboarding depends on accurate and consistent identity, contact, risk, and product eligibility data. Governance helps by:

Standardizing required fields and validation rules

Defining ownership for customer master data

Setting quality checks for missing or conflicting records

Clarifying retention and consent rules

Supporting auditability of onboarding decisions

When governance is weak, onboarding delays rise, duplicate profiles multiply, and downstream servicing becomes harder.

KYC and AML monitoring

KYC and AML processes rely on consistent customer, transaction, beneficial ownership, and alert data. Governance supports these processes through:

Common definitions across business lines

Controls on source system mapping

Quality rules for mandatory compliance attributes

Lineage for suspicious activity and case management data

Clear ownership for remediation

This is a strong starting point for beginners because the regulatory importance is obvious and the business case is easy to explain.

Credit risk

In lending environments, governance improves confidence in inputs such as:

Borrower identity and exposure

Collateral values

Default status

Delinquency measures

Internal and external credit attributes

If different teams use different definitions of exposure, default, or performing status, risk reporting becomes unreliable. Governance establishes common standards so portfolio, finance, and risk teams work from the same view.

Regulatory reporting

Regulatory reporting is one of the clearest proofs of governance maturity. It requires:

A governed operating model reduces last-minute reconciliation and strengthens confidence during internal and external review.

Enterprise consistency across products and channels

Financial institutions often grow through mergers, new products, and channel expansion. That creates inconsistent definitions across retail, corporate, digital, and branch operations.

Governance creates a common language across business units. For example, it helps align:

Customer

Account

Exposure

Revenue

Product hierarchy

Region

Delinquency

Loss event

This consistency is essential for enterprise reporting and board-level decision-making.

Impact on auditability, models, and reporting

Governance improves three areas that matter to executives:

Auditability: Teams can explain who owns data, how it changed, and what controls were applied.

Model inputs: Risk and pricing models receive more consistent and documented inputs.

Enterprise reporting: KPI definitions become stable, comparable, and easier to trust.

This is also where modern analytics platforms can add value. If governed data definitions are embedded in dashboards and semantic layers, tools like FineBI can help business teams explore performance faster without creating conflicting versions of key metrics.

A Practical Step-by-Step Approach to Data Governance Financial Services for Beginners

Many firms delay governance because they assume they need a large program, expensive tooling, or a full enterprise redesign. They do not. The best beginner approach is targeted, business-led, and incremental.

Assess the current state

Start by understanding the current environment. Focus on facts, not assumptions.

Review:

Critical data domains such as customer, account, transaction, product, risk, and finance

Major reporting and regulatory dependencies

Known data quality issues

Existing policies and standards

Current ownership model

Manual workarounds and reconciliations

Pain points raised by audit, compliance, finance, risk, and operations

A simple current-state assessment should answer:

Which data matters most?

Where are the highest risks?

Who currently makes data decisions?

What policies exist today?

Where are the biggest gaps in control or accountability?

Do not try to assess every dataset. Prioritize what is critical to the business and regulators.

Start with a focused scope

One of the most common failures in data governance financial services initiatives is trying to govern everything at once.

Keep the documentation simple and usable. If people cannot understand or locate it, they will ignore it.

A lightweight governance pack often works better than a complex framework in the early stages.

Improve over time

Governance maturity builds through repetition. After the first scope is working, create a roadmap for expansion.

Typical next steps include:

Extending stewardship to new domains

Improving metadata and business glossary coverage

Automating quality monitoring

Expanding lineage documentation

Formalizing governance forums

Training business and operations teams

Integrating dashboards for monitoring and adoption

This is where reporting maturity becomes important. Leaders need visibility into quality trends, issue backlogs, ownership coverage, and policy compliance. BI environments can support that visibility well when fed by governed definitions and workflows.

A practical roadmap should usually cover four tracks:

Common Challenges of Data Governance Financial Services and What Success Looks Like

Data governance is straightforward in theory but difficult in practice because it changes behavior, accountability, and decision-making.

Common challenges

Resistance to change

Teams often see governance as bureaucracy. They worry it will slow delivery or add more approvals. The solution is to show how governance reduces rework, confusion, and regulatory risk rather than adding unnecessary overhead.

Fragmented technology

Financial institutions often operate across legacy platforms, acquired systems, spreadsheets, and vendor tools. Governance cannot remove this complexity overnight. But it can create common definitions and control points that make fragmentation more manageable.

Overlapping responsibilities

Risk, compliance, IT, finance, operations, and business teams all touch data. Without a clear model, responsibilities overlap or fall through gaps. Governance clarifies who decides, who executes, and who challenges.

Limited executive sponsorship

Governance without leadership support becomes a documentation exercise. The program needs executive backing because ownership conflicts, funding needs, and policy enforcement usually cross business lines.

Trying to solve everything with tools

Tools help, but tooling is not governance. A catalog, lineage platform, or dashboard cannot compensate for missing ownership or undefined standards. Technology should support the operating model, not replace it.

What success looks like

A successful data governance program in financial services usually has these traits:

Critical data domains have named owners

Key terms are defined and used consistently

High-risk data quality issues are visible and tracked

Reports and models are easier to explain and defend

Access reviews happen on schedule

Escalation paths are known and used

Audit and regulatory conversations become more evidence-based

Business teams trust shared metrics more than local spreadsheets

Success does not mean perfection. It means the institution can identify, govern, monitor, and improve the data that matters most.

A simple checklist to begin

Use this checklist to launch a smart and practical governance effort:

Identify one high-value financial services use case to start with

Set a small number of quality rules and thresholds

Create a simple issue logging and escalation process

Review access permissions for sensitive data

Document basic lineage for key reports or controls

Track a few governance KPIs monthly

Expand only after the first scope shows measurable value

Data governance in financial services is not just a compliance exercise. It is a business operating capability. When done well, it lowers risk, improves reporting, strengthens trust, and creates a more scalable foundation for analytics, automation, and growth.

For beginners, the smartest move is not to build a massive framework on day one. It is to start where the business pain is real, define ownership clearly, publish practical rules, and measure improvement. That is how a governance program earns credibility.

And once that trust foundation is in place, institutions are in a far stronger position to unlock value from reporting, dashboards, and self-service analytics across the enterprise.

FAQs

It is the set of rules, roles, and controls that helps financial institutions define, manage, protect, and trust their data. In practice, it clarifies what important data means, who owns it, who can use it, and how issues are fixed.

They rely on accurate, secure, and traceable data for reporting, risk decisions, customer service, and regulatory obligations. Strong governance reduces errors, supports audits, and improves confidence in business decisions.

Data governance sets decision rights, standards, and accountability. Data management handles the day-to-day execution, while compliance focuses on meeting legal and regulatory requirements.

Responsibility is usually shared across business and data teams, including data owners, data stewards, and governance leaders such as a Chief Data Officer. The key is clear accountability for definitions, quality, access, and issue resolution.

Start small by identifying critical data elements, assigning owners, and defining a few practical standards for quality, access, and issue handling. Then build from there with simple policies, monitoring, and regular review rather than trying to govern everything at once.

Product Trial

FineReport

Pixel-perfect reports · Interactive dashboards · Easy data entry · Digital twins