You use the cost of goods sold formula to find out how much your business spends to make or buy the things you sell. The formula is:

COGS = Beginning Inventory + Purchases During the Period – Ending Inventory

When you figure out cost of goods sold, you see your costs clearly. This helps you choose prices, keep track of inventory, and check your profits. If you watch COGS closely, you can find problems and plan your money better. FineReport from FanRuan lets you do these calculations automatically and see your data, so making smart choices is easier.

What Is the Cost of Goods Sold?

The cost of goods sold formula shows what you spend on products. It helps you know how much money goes into making or buying things. Tracking cost of goods sold helps you see your business costs. You can notice patterns, pick prices, and handle inventory better.

Tip: Using smart tools like FineReport helps you manage financial data better, especially when things change fast in the economy. Click the demo to engage.

This formula matters for every business. If you make things, you count raw materials, labor, and overhead. If you run a store, you look at what you buy and sell. Service businesses add costs for giving their services. Each type of business uses the formula in its own way.

Tip: Keep good records of inventory and purchases. This helps you figure out COGS right and avoid errors.

The cost of goods sold formula has three main steps. First, you start with beginning inventory. Next, you add what you buy during the period. Last, you subtract ending inventory. Here is a table that explains each part:

You use this formula to find COGS for any time. It works for months, quarters, or years. If you want to check costs for a project, use the same formula. Just focus on items and purchases for that project.

The cost of goods sold formula can include other things. You might need to add raw materials, labor, and overhead. Here are some items you may count:

- Raw materials

- Labor costs for making products

- Factory or lab overheads (like rent)

- Parts and tools used in production

If you make products, your formula is more detailed. You add direct costs like materials and labor. In stores, the formula is simpler. You just add purchases and subtract ending inventory. Service businesses may add extra costs for giving services.

You should use the cost of goods sold formula the same way each time. If you change your method, your results may be different. You could miss patterns. Rules say you must report COGS in your financial statements. You need to show costs for each revenue type and keep your methods the same every period.

Here is a table with common mistakes when figuring out COGS:

Note: Always count all costs, even small ones, and use the same inventory method. This helps you avoid mistakes and makes your financial reports clear.

You can use FineReport by FanRuan to make COGS reporting easier. FineReport connects to your data, gathers inventory and purchase info, and figures out COGS for you. You can see results right away, make custom reports, and share them with your team. This saves time and helps you make smart choices.

If you want to compare your COGS to others, use this table:

When you use the cost of goods sold formula and tools like FineReport, you get a clear look at your costs. You can watch your spending, set better prices, and grow your profits.

Included in COGS

When you figure out cogs, you must know what costs to count. These costs show how much your business spends. Only count costs that go straight into making or buying products. This step helps you value your inventory the right way.

Here are the main things you include in cogs:

- Cost of items you want to sell again

- Cost of raw materials for your products

- Cost of all parts used to make each product

- Cost of direct labor, like workers who build products

- Supplies used to make or sell the product

- Overhead costs, like electricity or water for your factory

- Freight or shipping costs to bring materials to your site

- Container costs for storing or shipping products

- Some indirect costs, like sales force and distribution costs

These costs help you see your inventory value clearly. Each cost shows what you spend before selling a product. If you track these costs well, your cogs reports will be correct. This makes your inventory value stronger and helps you make smart choices.

Tip: Always keep records of every cost for your products. Good records make cogs and inventory value easier.

Excluded from COGS

Not every business cost goes in cogs. Leave out costs that do not connect to making or buying products. This keeps your inventory value right and your financial reports clear.

Here are the main costs you leave out of cogs:

- Selling, general, and administrative expenses (SG&A)

- Research and development (R&D) costs

- Non-manufacturing costs, like office rent or marketing

Do not count these costs in cogs because they do not change with how many products you make or sell. If you add these costs by mistake, your inventory value will not show the real cost. Always check your cogs calculation to make sure you only include the right costs.

Note: Check your expenses often. This helps you keep your cogs and inventory value correct.

Step-by-Step Guide

You can figure out cogs for your business by following some easy steps. This helps you see your costs and make better choices. Here is a simple guide for finding cogs:

- Find Beginning Inventory

First, look at your inventory at the start of the period. This number should be the same as the ending inventory from last time.

- Add Purchases During the Period

Next, add up all the costs for buying or making goods. Include raw materials, direct labor, and anything you bought to sell. Do not count indirect costs like office rent.

- Determine Ending Inventory

Then, check how much inventory you have left at the end. You can use FIFO, LIFO, or Weighted Average to figure this out.

- Apply the Formula

Now use the cost of goods sold formula:

COGS = Beginning Inventory + Purchases - Ending Inventory

This gives you the total cogs for the period.

Tip: Update your cogs calculation often. If your business sells a lot, you might use a perpetual inventory system. This updates cogs right away. If you have fewer sales, you might use a periodic system and update cogs at the end of each period.

Here is a table that shows how often to update cogs based on your inventory system:

Example Calculation

Let’s look at an example to help you understand how to find cogs. Imagine you own a small shop that sells coffee mugs.

- You start the month with 100 mugs in inventory.

- You buy 200 more mugs during the month.

- At the end of the month, you have 50 mugs left.

Here is how you find cogs:

- Beginning Inventory: 100 mugs

- Purchases: 200 mugs

- Ending Inventory: 50 mugs

Use the formula:

COGS = Beginning Inventory + Purchases - Ending Inventory

COGS = 100 + 200 - 50

COGS = 250 mugs

Now, let’s add the cost for each mug. You paid 5forthefirst100mugs,6 for the next 100, and $7 for the last 100 mugs.

- 100 mugs x 5=500

- 100 mugs x 6=600

- 100 mugs x 7=700

Total cost: 500+600 + 700=1,800

Total mugs: 300

Weighted average cost per mug: 1,800/300=6

Your cogs for the month:

COGS = 250 mugs x $6 = $1,500

Note: When you find cogs, always count direct costs like materials, labor, and freight. Do not include overhead or marketing costs.

Seasons can change your cogs calculation. If you use FIFO, you sell older items first, which is good for things that can spoil. LIFO can make cogs higher when prices go up, which can lower taxes. Weighted average helps keep prices steady.

Calculate Cost of Goods Sold with FineReport

You can make finding cogs easier by using FineReport from FanRuan. FineReport connects to your inventory and purchase data, so you do not have to type in numbers. You can set up automatic cogs calculations for each period. The software updates your reports right away, so you can track costs and inventory.

FineReport lets you:

- Bring in data from Excel or other places.

- Use easy tools to make custom cogs reports.

- See your cogs on dashboards and share with your team.

- Set up automatic updates, so your cogs reports are always current.

- Look at details, like costs for each product or project.

Tip: With FineReport, you can see trends in your cogs and make smart choices about prices, inventory, and spending. You save time and make fewer mistakes by letting the software do the math.

If you want to find cost of goods sold for different times or projects, FineReport lets you do that. You can compare cogs for months, quarters, or years. You can also see how seasons change your costs and change your plans.

FineReport helps you keep your cogs calculation correct and up to date. You get clear reports that help you make better choices for your business.

When you figure out cogs, you must pick an inventory method. The method you choose changes how you show costs and profits. Here is a table with the main inventory methods:

FIFO

FIFO means "First in, First out." You sell the oldest inventory first. This puts the oldest costs into cogs. When prices go up, FIFO gives you lower cogs. Your profits look higher, which can help your business. You might pay less tax. FIFO matches old costs with your sales, so your inventory shows newer prices.

- FIFO puts the oldest costs in cogs first, so cogs are lower when prices rise.

- This means you report higher profits, which can help your cash flow and taxes.

- FIFO matches income with old costs, so you can save money or pay bills.

LIFO

LIFO stands for "Last in, First out." You use the newest inventory first for cogs. If prices go up, LIFO gives you higher cogs. This makes your profits lower and your taxes smaller. LIFO matches what you pay now with what you sell now. Your inventory shows older prices on your balance sheet.

- LIFO lowers your taxable income when prices rise, so profits and taxes are lower.

- FIFO usually gives higher profits and higher taxes because it uses old costs.

- LIFO matches today’s sales with today’s costs, so cogs are more accurate.

- Higher cogs with LIFO means lower profits, so you might save on taxes.

Weighted Average

Weighted Average adds up all your inventory costs and finds the average. Every item uses this average cost in cogs and inventory. This keeps your numbers steady, even if prices change. You do not need to track each item’s cost. Here is a table with the good and bad points:

Tip: Choose the inventory method that works best for your business. Each method changes your cogs, profits, and taxes. If you use FineReport, you can see how each method changes your reports.

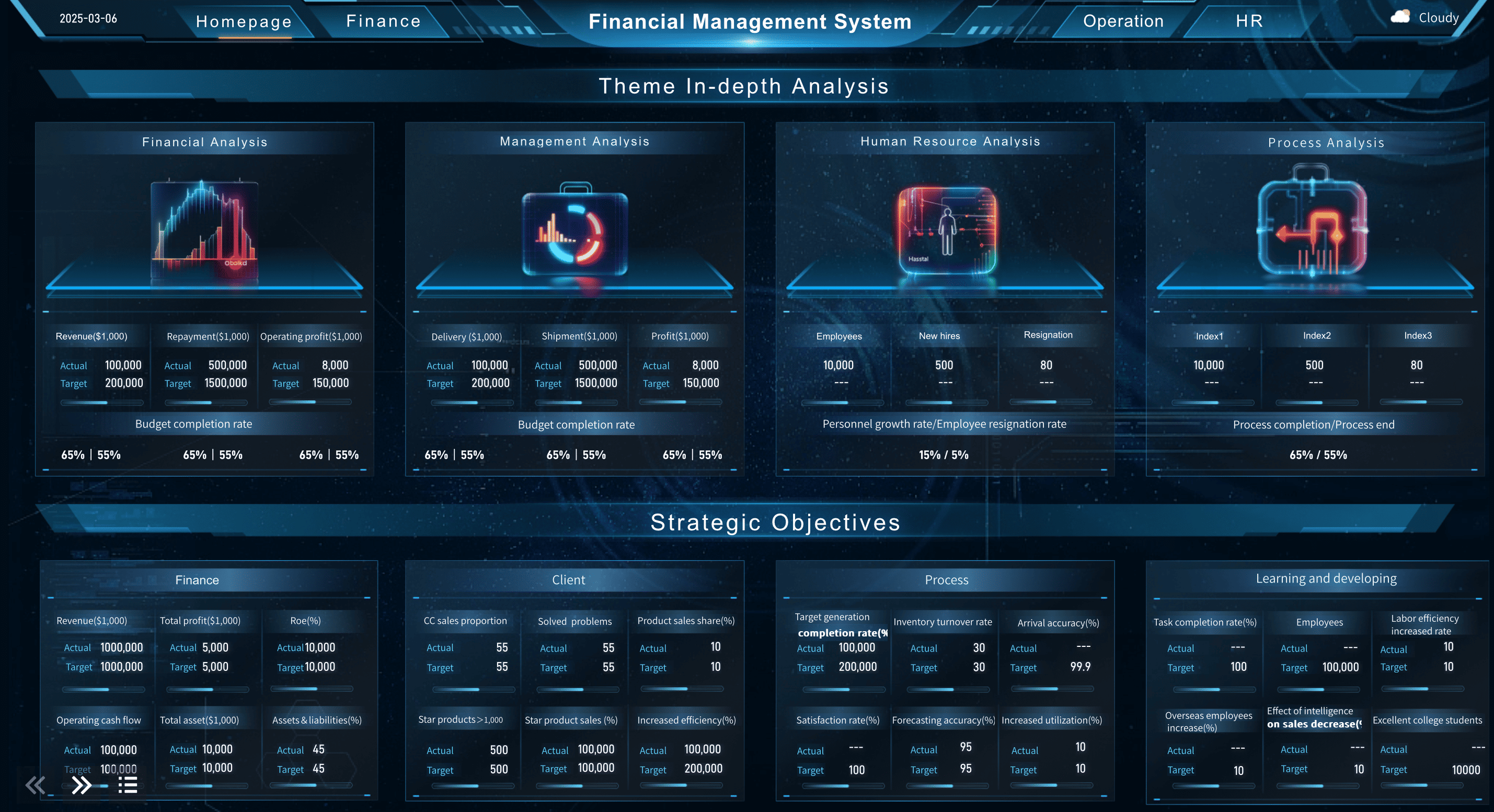

Financial Analysis

You need to know cogs to see how your business is doing. Cogs is very important when you look at your money. When you take away cogs from your sales, you get gross profit. This is called finding your gross profit. It shows if your business can pay other bills and still earn money. If cogs gets higher, gross profit gets lower. This change affects your gross margin and shows if you control costs well. You can use cogs to check if your prices are good or if you need to spend less.

Here is a table that shows how cogs changes your business:

Profitability and Taxes

Cogs changes how much profit and taxes you have. If you figure out cogs the right way, you see your real profits. If you say cogs is too high, profits look smaller. If you say cogs is too low, profits look bigger, but you might pay more taxes or get in trouble. Getting cogs right helps you know your profits and plan for taxes.

- Getting cogs right helps you find taxable income and pay less tax.

- You can take away cogs from your income, so you owe less tax.

- How you track inventory, like FIFO or LIFO, changes cogs and taxes.

- Good inventory tracking helps you report cogs right and avoid tax trouble.

- If you get cogs wrong, you could get checked, fined, or lose trust.

Note: Always check your cogs numbers. Mistakes can give wrong profits and tax problems.

Using FineReport for COGS Insights

FineReport makes cogs easy to understand. FineReport connects to your data and updates cogs reports right away. You can see patterns, compare times, and find problems fast. The software lets you make dashboards to watch cogs, profits, and inventory in one spot.

With FineReport, you can:

- Get data from many places to see all cogs.

- Make reports that show how cogs changes over time.

- Look closer at cogs for each product or project.

- Share what you learn with your team to help make choices.

FineReport helps you stop mistakes and keeps cogs reports current. You get a better look at your business, so you can earn more and be ready for taxes.

When you know your cost of goods sold, you see what your business really spends. COGS changes your gross profit, helps you set prices, and lets you control inventory. Many businesses have problems like mistakes from tracking by hand, prices for materials that change, and hard-to-manage inventory. FineReport from FanRuan puts all your data in one place, does the math for you, and shows results on simple dashboards.

Look at how you figure out COGS. Digital tools like FineReport help you work better and help your business grow.